E3’s 2026 Core Case Electricity Market Price Forecasts are now available off-the-shelf for every major North American power market, including (for the first time) Ontario’s IESO.

These forecasts are the product of thousands of hours of production cost modeling, reliability analysis, and real-world transaction support. They are based on market fundamentals and built from the ground up using detailed assumptions about load growth, fuel prices, resource costs, state and federal policy, transmission constraints, and market rules.

E3’s forecasting approach is driven by our twin guiding principles:

(1) To create a flagship product supported by rigorous, fundamentals-based analysis that is developed with great care, foresight, and thought in a transparent and intellectually honest manner; and

(2) to provide a “consultant-first” engagement platform built on our cross-cutting and best-in-class expertise in the industry. Every single member of E3’s forecasting team is actively involved in our complex, client-facing consulting work, so the product reflects both on-the-ground realities as well credible and defensible forward looking views.

Across markets, three forces are reshaping prices:

- Load growth: data centers, electrification, and industrial transformation are changing peak demand and hourly load shapes.

- Increased resource costs: the 2026 edition incorporates our latest outlook and market data on the costs of new resources, including costs of new gas turbines and updated expectations of import tariffs and FEOC rules impacting solar, wind, and storage projects.

- Gas prices: elevated expectations of long-term gas demand drive up fuel prices over the forecast horizon.

Forecast outputs include:

- Day-ahead energy | hourly x zone x 30 years

- Real-time energy | hourly x zone x 30 years (sub-hourly intervals available on request)

- Ancillary services | hourly x zone x 30 years for each market product

- Resource Adequacy (RA) / Capacity | annual by zone x 30 years

- Renewable attribute values (RECs) | annual by region x 30 years

- Documentation of assumptions: Load growth, fuel prices, technology costs, retirements, policy drivers, and transmission constraints.

These forecasts are used for underwriting, procurement, planning, strategy, and investment. They have supported billions of dollars of transactions across solar, wind, storage, gas, offshore wind, and transmission. We view these as flagship products which represent our latest market views made available off-the-shelf, but which can also be customized with tailored consulting support with nodal forecasts, technology-specific revenue modeling, or additional scenarios beyond the Core Case.

Market Highlights

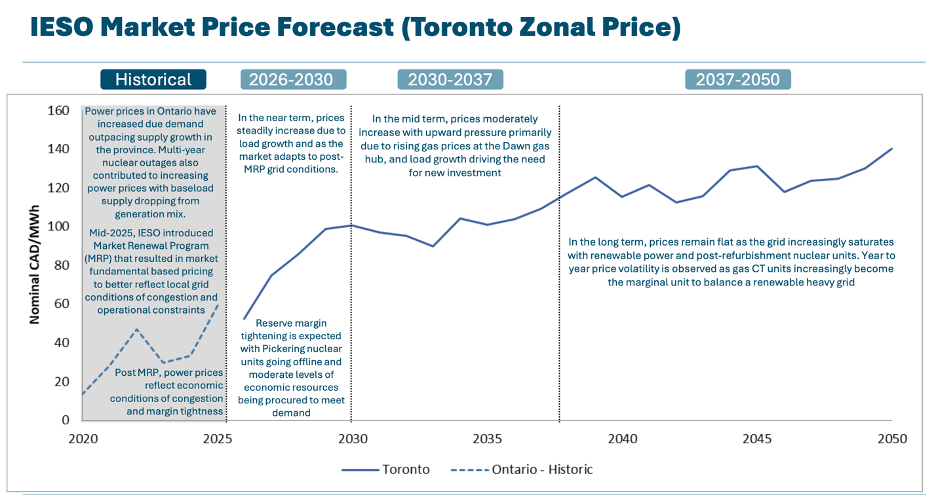

Ontario (IESO): new this year

This is the first year E3 is releasing an Ontario IESO forecast off-the-shelf.

Ontario is entering a fundamentally different era. After a decade of relatively flat demand, electricity use is accelerating. The IESO projects total demand growing from roughly 157 TWh in 2026 to over 260 TWh by 2050, with both summer and winter peaks rising materially, meaning a true dual-peaking system.

At the same time, the market itself has changed. In May 2025, the IESO implemented the Market Renewal Program (MRP), introducing locational marginal pricing (LMP), a day-ahead market, and enhanced real-time commitment. Prices now reflect local congestion and system conditions across nearly 1,000 nodes.

Ontario is also managing the retirement of Pickering A nuclear units and multi-year refurbishments at Bruce, Darlington and Pickering B. That reduces baseload supply at the same time that industrial electrification, EV charging, and data centers increase demand. In the near term, that combination pushes prices higher and increases sensitivity to peak conditions.

Over the longer term, our modeling shows:

- Significant additions of wind and storage as economic resources.

- Gas remaining important for flexibility and reliability.

- Price volatility increasing as renewables take a larger share of the generation mix and gas units increasingly set the marginal price in peak hours.

IESO sample price forecast and sample report >

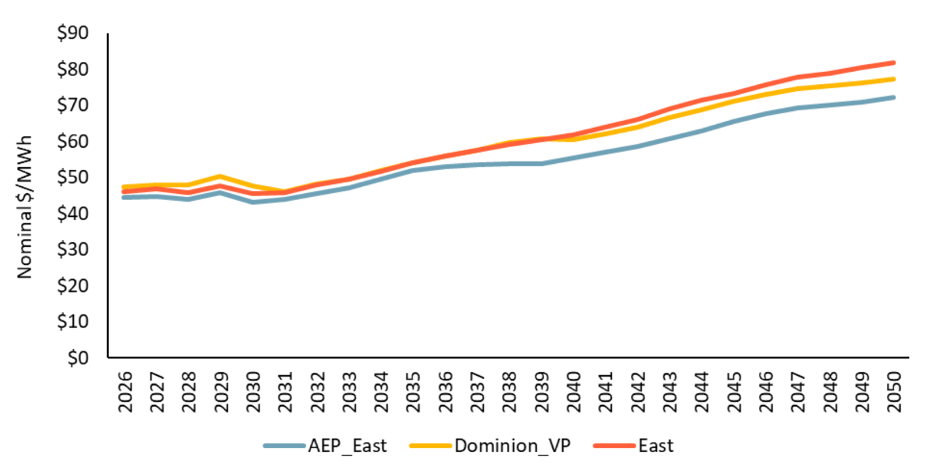

PJM: the data center hub

Northern Virginia has become the largest data center market in the world, and new large-load interconnection requests continue across PJM. PJM is planning around sustained, large, and often inflexible demand increases.

This new demand is arriving as older coal plants retire and the resource mix shifts toward solar, wind, storage, and gas. At the same time, PJM has changed how it measures reliability contributions from each resource over a range of historical and potential future grid conditions.

Near term retirements and higher expected load growth keeps PJM tight on accredited capacity throughout the forecast horizon. Capacity prices remain elevated as the system continues to need new effective capacity to meet load growth and replace retiring plants, putting pressure on the capacity market to support the costs of new entry over an extended period.

Energy prices respond differently. In the near term, average annual energy prices remain relatively stable because gas prices are relatively flat and there is headroom in the existing generator fleet during most hours of the year. Over time, however, the same forces that are tightening the capacity market also begin to shape energy prices. As load continues to grow and gas prices rise, annual average energy prices also increase.

This year’s edition reflects these dynamics:

- Updated data center load growth embedded into hourly shapes and peak forecasts

- Updated reliability accreditation assumptions for renewables and storage under PJM’s current framework

- Considerations for political intervention to contain prices in the capacity market

- Renewable build assumptions based on what’s realistically moving through the interconnection queue

PJM sample price forecast and sample report >

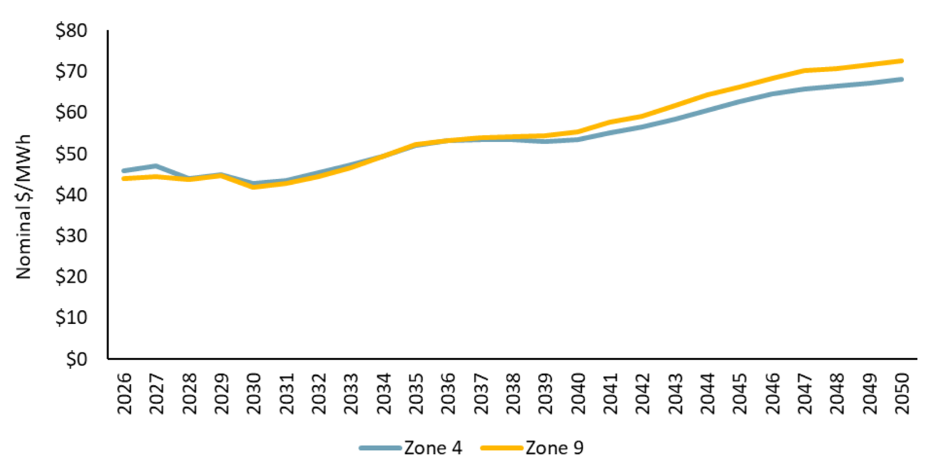

MISO: stable now, reliability risks later

In MISO, the near-term outlook looks relatively stable. Average annual energy prices do not move dramatically over the next few years because several forces are offsetting one another: coal plants are retiring, but new gas units and renewables are coming online; load is growing, but not yet faster than new supply. And near-term gas prices remain fairly flat, so average energy prices are stable.

However, this shifts materially in the 2030s. Load growth, particularly in MISO North, begins to accelerate at the same time as coal retirements and large new gas projects face multi-year interconnection and development timelines. In other words, dependable supply is leaving the system faster than new firm capacity can replace it.

The region also now accredits resources on a seasonal basis, meaning a plant’s capacity value depends on how available it is during the highest-risk hours of each season. As wind, solar, and storage perform differently across seasons, their effective contribution to reliability can decline even as total installed capacity rises.

In our Core Case:

- Capacity prices remain elevated into the early 2030s as the system works through retirements and delayed firm additions.

- Gas generation increases materially to replace retiring coal and provide reliability during peak conditions.

- Storage deployment accelerates, initially earning strong ancillary service revenues before those markets begin to saturate.

- Renewable attribute values decline as solar costs fall and energy revenues evolve.

MISO sample price forecast and sample report >

Forecasts are available for purchase directly through our website. You may download market-specific sample forecasts and reports here.

For questions, pricing, or tailored requests, contact marketprices@ethree.com.