It is well known that electricity bills have been climbing across much of the U.S., driven in part from increases in the underlying retail rates. Data centers, given their size and visibility, have become a focal point in public discussion of those increases, especially given their rapid and continued expansion. Retail rate outcomes, however, reflect many interacting factors, including generation, transmission, distribution, policy, market design, and load growth. The mix and magnitude of those factors differ across markets and customer classes, and the relationship between load growth and retail rates is more complex than the public conversation often conveys.

A new E3 whitepaper, Understanding the Drivers of Rising Electricity Rates and the Role of Data Centers, examines what the available quantitative evidence does and does not show about that relationship. Funded by the Data Center Coalition and independently authored by E3, the report draws on a review of 11 recent quantitative studies, interviews with 4 industry experts, and an original E3 analysis of PJM capacity auction outcomes.

The goal of this paper is to help fill an analytical gap by comparing and synthesizing the available research, providing a foundation for the public discussion on rising rates and the role of data centers.

Many factors are driving rate pressure, not just load growth. E3 identifies inflation, natural gas price volatility, resilience spending, grid modernization, and wholesale market design and supply dynamics as major contributors to recent rate increases. Data center load growth is one factor among several, and the relative weight varies by region.

The relationship between load growth and rising electric rates is unclear. The evidenceis mixed: state-level comparisons show that states with the largest load growth (e.g., Texas and Virginia) saw the smallest rate increases, while states with declining load growth (e.g., California and New York) saw the largest rate increases. A 2026 Lawrence Berkeley National Laboratory study reached similar conclusions outside the PJM footprint.

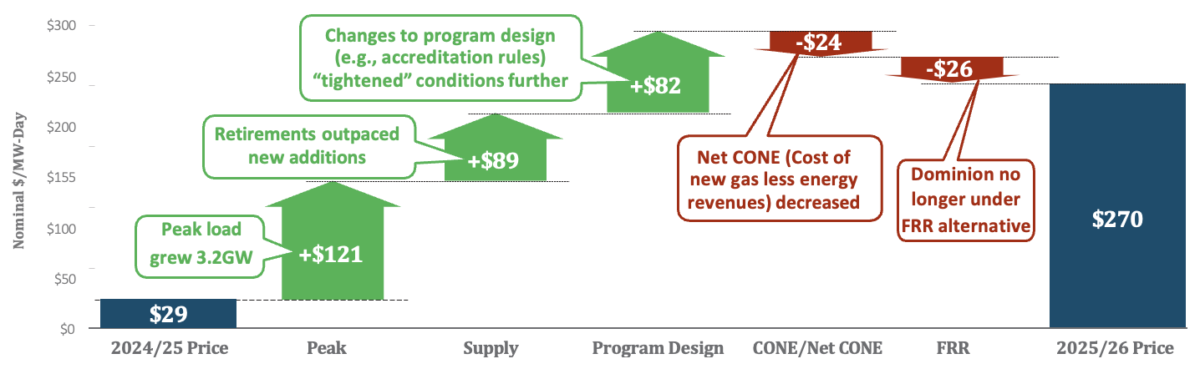

Even where load growth has clearly contributed to price pressure, isolating its specific impact is complicated. In PJM, E3’s analysis of the 2024/2025 and 2025/2026 capacity auctions attributed approximately 50% of the price increase to load growth, with the remaining 50% driven by market design changes, power plant retirements, reduced accreditation of fossil resources, and other supply-side factors. Capacity is also only one component of a residential bill, adding another step between wholesale market dynamics and the rates customers pay.

The quantitative studies reviewed do not show evidence of historical subsidization. E3’s prior study for Virginia’s Joint Legislative Audit and Review Commission (JLARC), in the world’s largest data center market, found no evidence of a historical cost shift from data centers to residential or small commercial customers.

Under the right conditions, large loads can lower rates for other customers. In an earlier facility-level analysis of Amazon data centers across four diverse utility territories, E3 found that each site, on average, generated roughly $3.4 million in net surplus revenue, as payments to the utility exceeded the incremental cost to serve the facility.

Regulatory tools must adapt to the rapid pace of load growth to continue protecting ratepayers. As load growth has accelerated, regulatory and policy tools have been adapting in kind, with at least 38 new large load tariffs established since 2018, 30 of them in 2025 and 2026 alone. This momentum should continue, but there is no “one size fits all” solution. Affordability outcomes depend heavily on market-specific contexts and frameworks, as illustrated by how PJM, Texas, Georgia, Arizona, and Missouri have each responded to rapid load growth in the report’s case studies.

To continue to manage growth and protect ratepayers, the report recommends strengthening planning and forecasting to limit speculative overbuild, expanding tailored large load tariffs with regular cost allocation updates, enabling innovative supply and load integration approaches such as “bring your own generation” and load flexibility, and closing remaining research gaps through targeted analysis.

Read the full report >

For further information on E3’s work on large loads and rate design, please contact kushal.patel@ethree.com.