E3 has released its 2025 edition Core Case electricity market price forecasts for every major North American market. These forecasts explicitly incorporate recent U.S. federal policy actions, spanning tax credits to tariffs, along with updated views on large load growth (such as data centers). They are a flagship product for our firm, built on over ten thousand hours of modeling and analysis and informed by our work across the energy sector, from policy and planning to procurement, asset valuation, and financing. Each forecast reflects a realistic, consistent, and fundamentals-based view of how policy, economics, technology, and demand will shape energy, capacity, ancillary service, and renewable attribute prices through 2055. All inputs and assumptions are fully documented and backed by industry leading expertise. View sample outputs and purchase forecasts here.

This year’s update incorporates the first full view of post–Budget Reconciliation Bill conditions. Across every market in the U.S., load growth remains a defining feature. The drivers are varied: rapid data center development, new industrial loads, continued (though slower) EV adoption, and higher air conditioning use as summers become hotter. In some markets, population growth adds another layer of demand.

Meeting this demand requires new generation. Gas turbines remain an important reliability resource, but manufacturing capacity is limited and order backlogs are long. Energy demand exceeds production rates of new turbines, raising costs in the near term and raising demand for new energy from all resources, including wind and solar, in a more turbulent and constrained development market.

Demand for energy (and renewable energy) remains strong across U.S. markets. In the short term, all available resources are needed to meet load growth. In the medium and long term, renewables will continue to support demand growth and to advance policy-driven energy transitions. Tariffs and tax policies raise the costs of imported equipment. At the same time, capacity markets and other reliability mechanisms are becoming more expensive as load growth exceeds current capacity and requires new generation and transmission resources to meet demand and maintain grid reliability.

The importance of capacity and grid reliability is increasing across all regions. Our 2025 forecasts capture these dynamics for each market, with updated views on resource costs, build constraints, and demand growth.

View sample outputs >

The sections that follow highlight several examples of how these conditions are reflected in specific markets, including Texas, New York, PJM, and California.

Market Snapshots

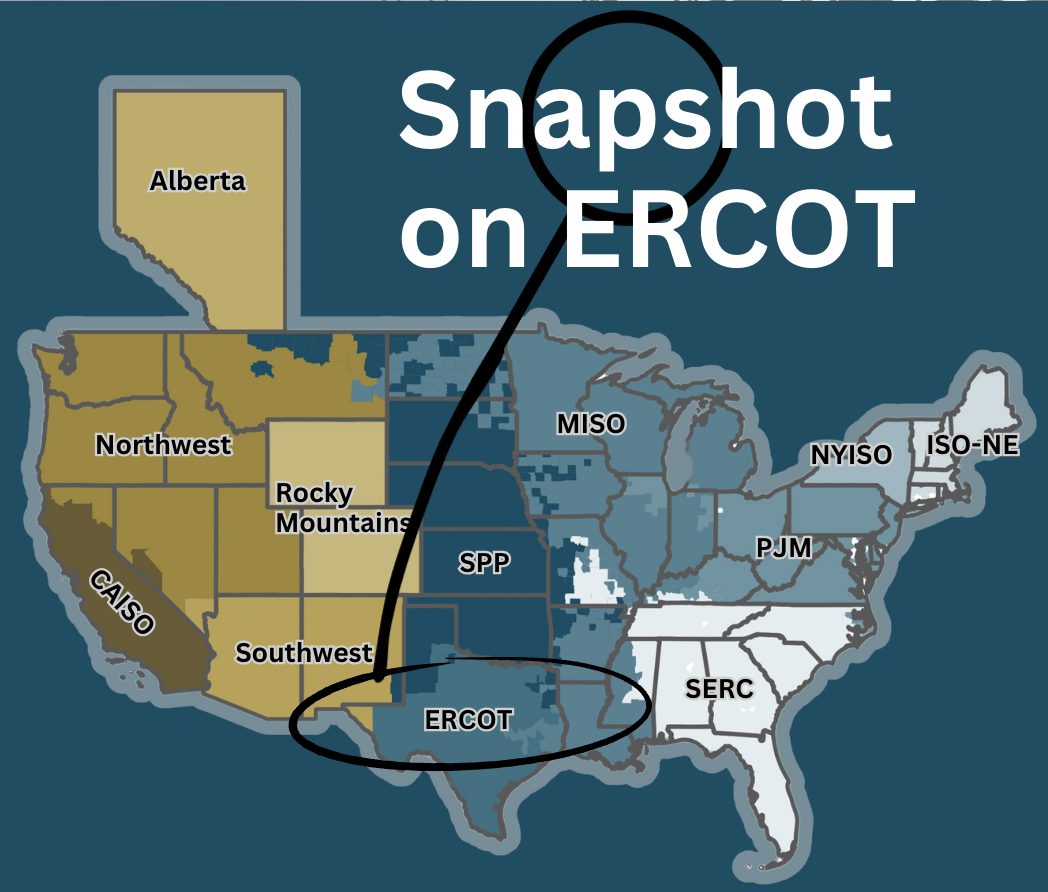

ERCOT (Texas)

After the passage of the Budget Reconciliation Bill, the phase out of tax credits for solar and wind result in lower deployments and a roughly $15/MWh increase in average annual energy prices from 2026 to 2035.

Near-term solar build remains strong as late-stage projects move forward, but market saturation limits the potential for price relief. Wind additions are constrained by the small number of shovel-ready projects in the queue, and wind and solar additions slow after safe harbor windows expire. As a result, gas generation doubles from 200 TWh in 2026 to 400 TWh by 2035. Battery storage deployments increase, supported by the extended credit timeline, but not at a scale sufficient to close the gap between supply and demand.

By 2035, prices in the new 2025 case are nearly $30 per megawatt-hour higher than our previous case (which assumed a 2032-2035 phaseout of renewable tax credits). These dynamics lead to a steeper run-up in prices and greater reliance on gas through the 2030s.

NYISO (New York)

For the remainder of this decade, E3 expects tempered energy and capacity prices in New York. This is due to the combination of delayed large thermal retirements and the completion of the CHPE transmission line delivering power from Quebec into New York City.

In the 2030s, conditions are expected to change. Several factors will drive price escalation, particularly in the capacity market: a resumption of thermal retirements, continued load growth, delayed offshore wind development linked to current federal policy, and a slowdown in battery deployment following the 2030 mandated buildout. These changes will tighten supply and create greater reliability challenges in the next decade.

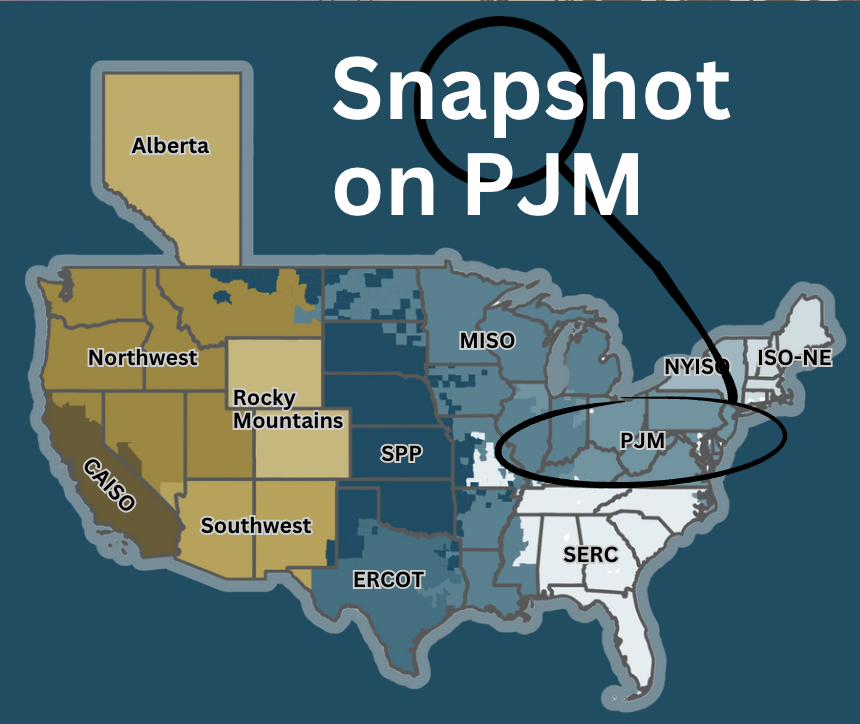

PJM

Data centers are the primary driver of anticipated long-term load growth in PJM. Northern Virginia already handles roughly 70% of global internet traffic, and regional data center demand is expected to increase sharply in the years ahead. Peak demand in 2024 reached levels not seen in nearly a decade.

Recent PJM capacity auctions have reflected this shift. The most recent auction cleared at the price cap, consistent with E3’s expectations. Higher prices are largely the result of large thermal retirements and the move to marginal capacity accreditation, which reduces the credited capacity of renewables, storage, and even dispatchable thermal units. This combination has tightened the capacity market.

Looking forward, the PJM capacity outlook will depend on the pace of load growth, the speed at which new firm resources replace retiring coal, and the ability of the existing thermal fleet, primarily gas, to improve availability during tight conditions. The interaction of these factors will influence both market prices and potential policy responses aimed at containing ratepayer impacts.

California and the West (CAISO and WECC)

The accelerated expiration of the ITC and PTC for solar, wind, and battery storage (combined with elevated tariffs) has increased projected costs for new resources significantly. Higher solar development costs will lead to elevated Renewable Energy Credit (REC) prices.

California’s policy-driven market continues to shape the resource mix. Solar and out-of-state wind dominate new clean energy additions, while battery storage procurement continues despite higher costs. Storage remains critical to meeting reliability needs and clean energy targets, consistent with the CPUC Integrated Resource Plan.

The launch of EDAM and Markets+ around 2026–2027 is expected to improve price transparency, liquidity, and efficiency in energy markets across the WECC. Actual impacts will depend on the participation of individual balancing authorities and whether they are net exporters or importers.

E3’s forecasts are available off-the-shelf for all major markets and can be customized for nodal granularity, alternative scenarios, and transaction-specific needs. They are designed to support investment decisions, procurement planning, and policy analysis.

Browse forecasts and sample outputs or contact us at marketprices@ethree.com to discuss your specific needs.