On June 24th the CPUC approved the 2021 update to the Distributed Energy Resources Avoided Cost Calculator (ACC) in a 5-0 vote. This normally obscure approval via the resolution process (Resolution E-5150) garnered a lot of public comment arguing that the decline in avoided costs from 2020 would harm the rooftop solar industry. After listening to public comment, the commissioners unanimously stood by the recommendation of Energy Division, NRDC, TURN and CalAdvocates to approve the new avoided costs.

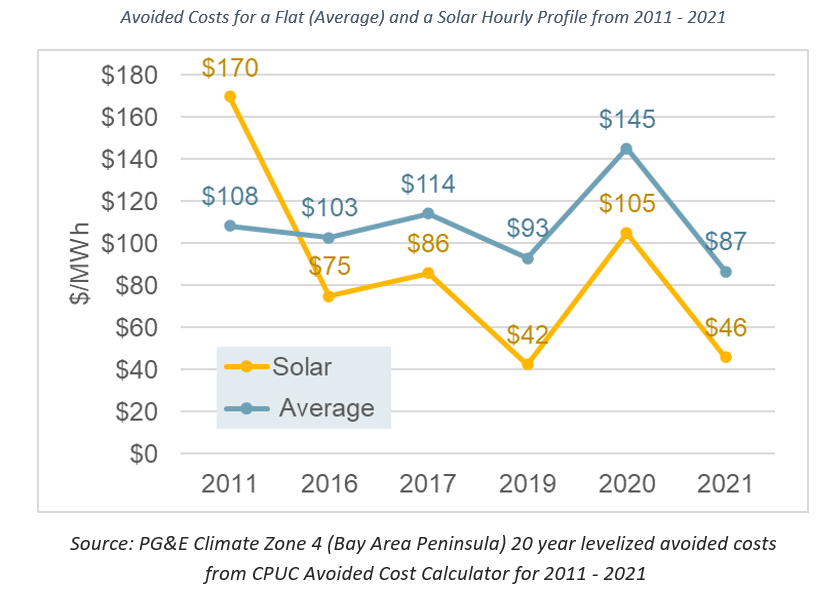

The ACC is the model developed by Energy and Environmental Economics (E3) under contract with the CPUC to determine the value DER. In 2020 the CPUC and E3, with significant stakeholder input, implemented a major update to better and align supply and demand side planning in the CPUC’s efforts to realize a reliable, zero carbon electric grid at the lowest possible cost to ratepayers. The 2020 update implemented a number of new models and methods and for the first time in many years, resulted in an increase in avoided costs for DER. In 2021, those models were improved and calibrated to better reflect conditions observed in the market as solar penetration increased in California, and a number of inputs were updated to more recent (and lower) cost estimates for solar and storage technology. This significantly lowered the avoided cost value relative to 2020 for solar in particular, but put the ACC back on track to be consistent with the long-term trend of declining costs for zero carbon generation in California.

The Declining Cost of Solar (and Storage) is a Success Story for California

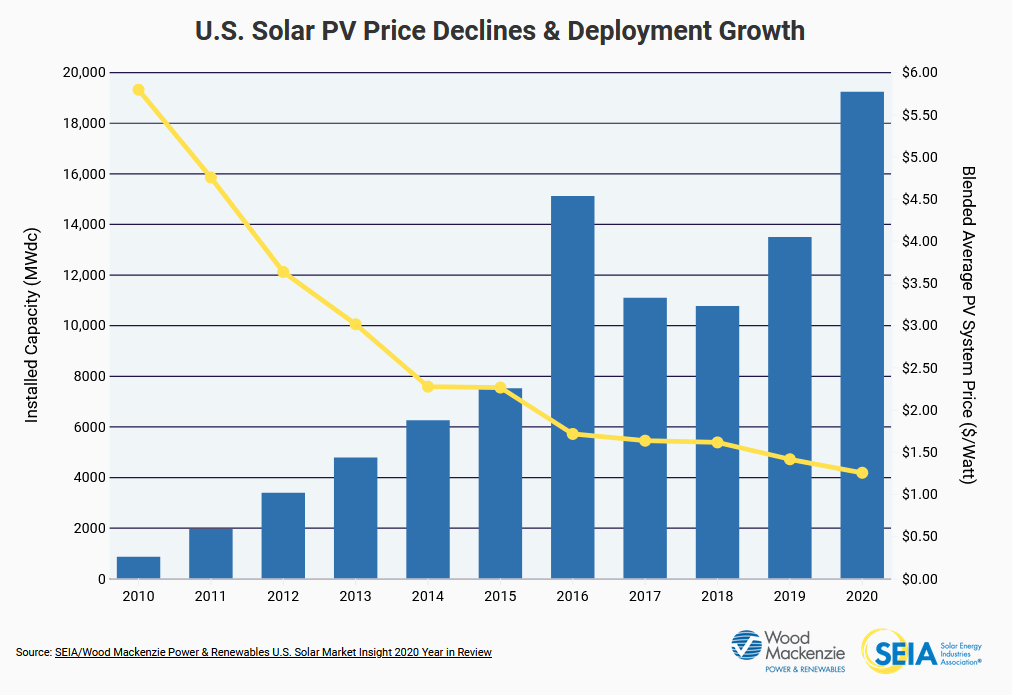

The success of the solar industry, driven in part by the success of market transformation policies in Germany and California, has been remarkable. Rapidly declining costs have led to dramatic increases in the GW of solar installed. Source: https://www.seia.org/solar-industry-research-data

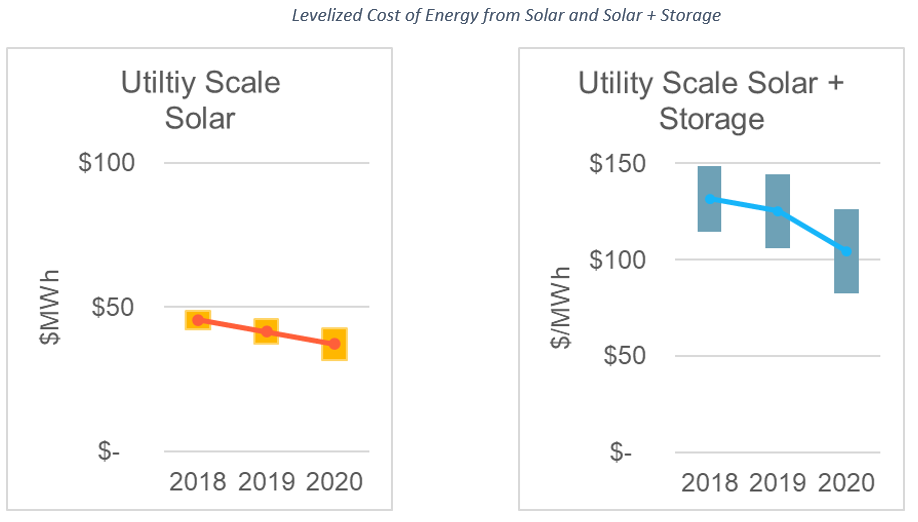

The costs of energy storage have been declining rapidly too. This is a positive story for California as solar and solar + storage projects have become competitive against traditional fossil fuel generation and the preferred resource for California to provide zero carbon electricity. Source: https://assignmentbro.com/wp-content/uploads/2023/12/cost-of-energy-report.pdf

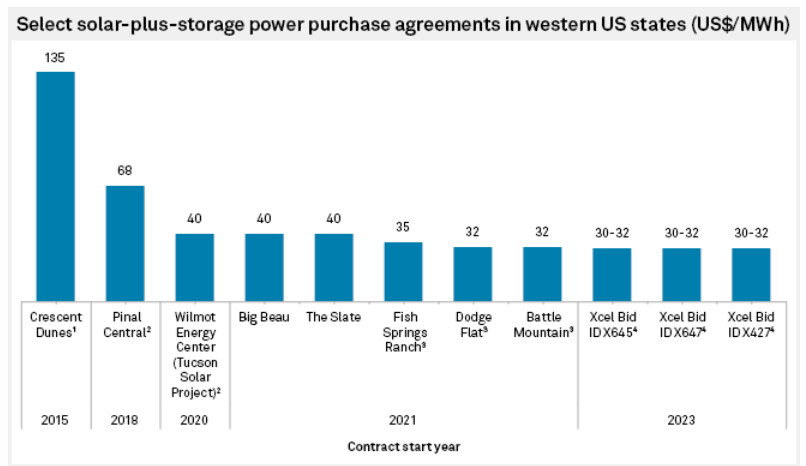

The prices utilities pay for solar + storage power purchase agreements are also falling. Source: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/us-solar-plus-storage-prices-plunge-in-utility-contracting-surge-51328301

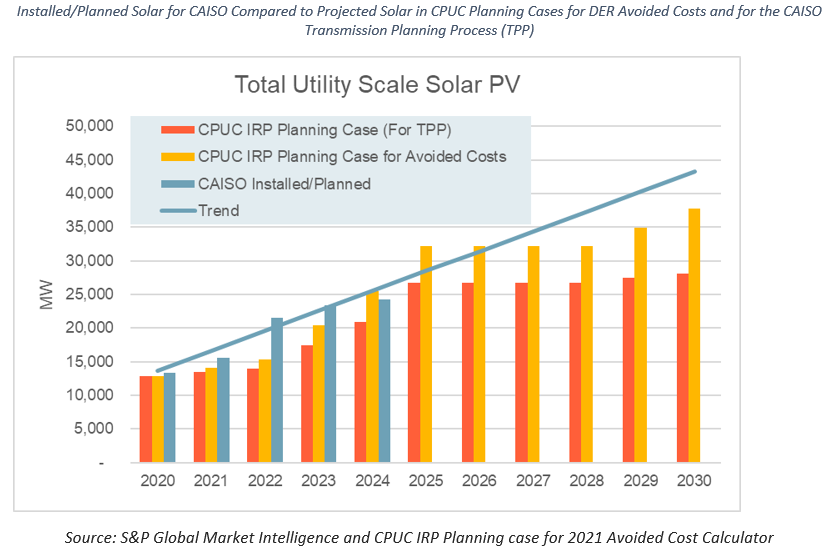

As a result, California is on track to have more than 35 GW of solar by 2030. The graph below shows the total MW of utility scale solar installed or planned in CAISO (in blue, from S&P Global Market Intelligence), compared to the total installed solar assumed in the CPUC IRP planning case for the Avoided Costs (in yellow). Note that this graph shows the total planned supply side solar for a “No New DER” case that is used exclusively as an input for the Avoided Costs. The actual CPUC IRP planning cases designed to meet California’s clean energy goals have a lower solar build (the latest case, shown in orange below, was developed for the CAISO Transmission Planning Process (TPP) and published in January 2021).

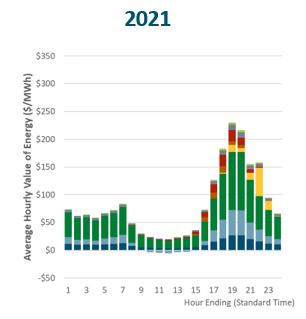

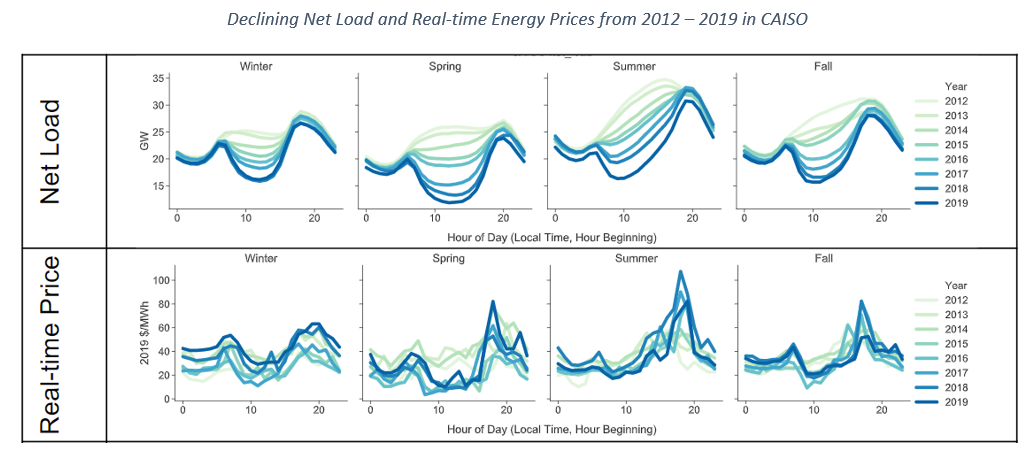

Increasing Solar Generation is Lowering Energy Prices

The increase in solar generation is already leading to a dramatic increase in the supply of energy during the day. As basic economics would suggest, this increase in supply is lowering energy prices during the hours of the day when solar is generating.

Source: LBNL https://emp.lbl.gov/renewable-grid-insights and https://emp.lbl.gov/publications/solar-and-wind-grid-system-value

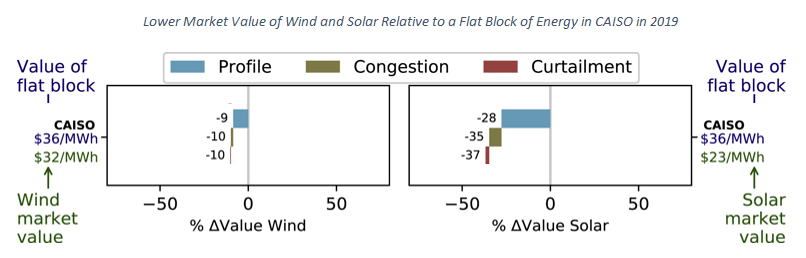

Declining costs and increasing deployment creates a challenging feedback loop for solar – as more solar and solar + storage is installed, its price in the market and value as a resource in zero carbon electricity planning declines.

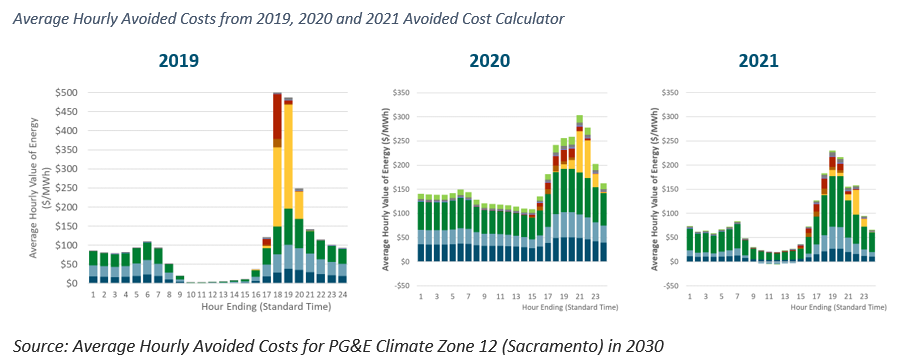

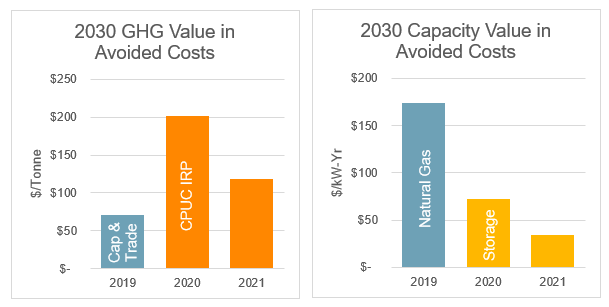

The 2021 Avoided Costs are robust and in line with industry trends

2020 (not 2021) was the first time using a dramatically revised ACC methodology that increased consistency between the IRP and IDER ACC proceedings. The first time using the CPUC’s production simulation model led to some counter intuitive results and 2020. The 2021 update is more inline with historical avoided costs and observed market trends

The 2020 update improved alignment with the CPUC Integrated Resources Planning (IRP) and Distribution Resources Planning (DRP) proceedings to better align supply and demand side planning. For example, the 2020 ACC dramatically increased the $/ton value for GHG from 2019 based on IRP modeling, but declining solar and solar + storage costs have reduced that value in 2021. Another change was the benchmark for capacity value becoming 4-hour energy storage in place of a natural gas combustion turbine. This lowered the avoided cost value for capacity in most years, which declined further with lower storage costs in 2021.

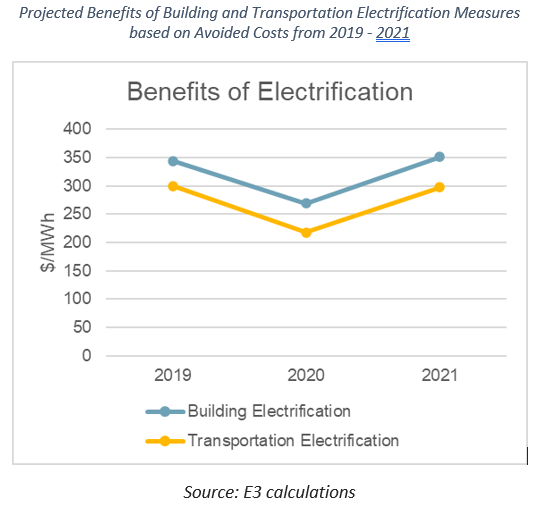

The 2021 Avoided Costs reduce the value energy efficiency and demand response as well as solar. On the other hand the benefits for both building and transportation electrification increase, each a key pillar for California’s economy wide decarbonization strategy.

This article was originally published by Eric Cutter on LinkedIn and updated on September 28, 2021.